Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Weekly Market Pulse: Look Up In The Sky! It’s A UFO! Or Not!

Weekly Market Pulse: Look Up In The Sky! It’s A UFO! Or Not!13 Feb 2023

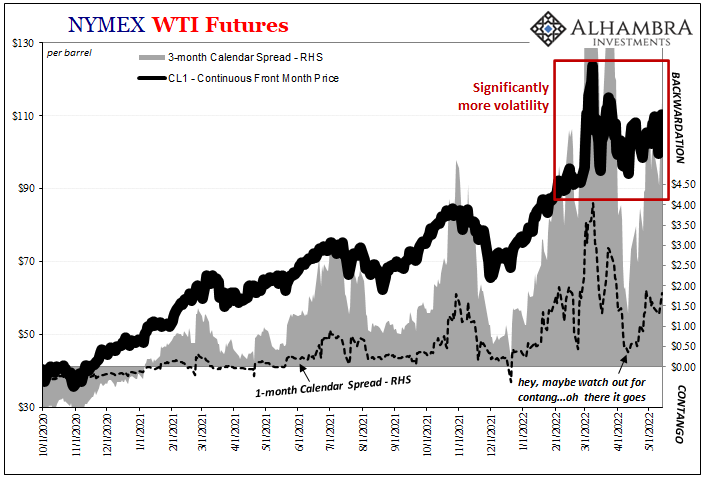

Crude Contradictions Therefore Uncertainty And Big Volatility18 May 2022

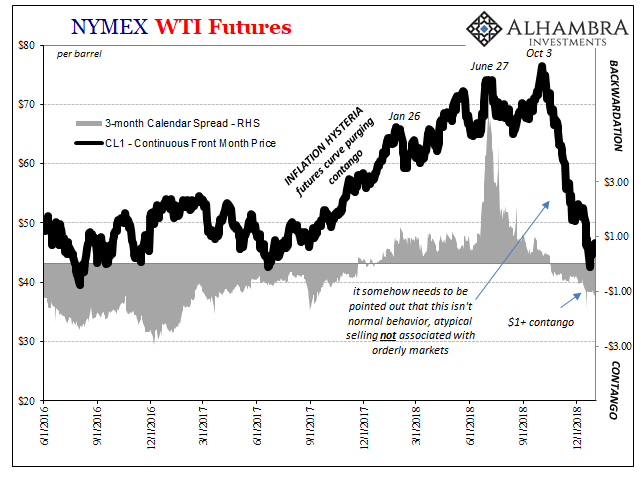

Inflation Hysteria #2 (WTI)

Inflation Hysteria #2 (WTI)12 Dec 2020

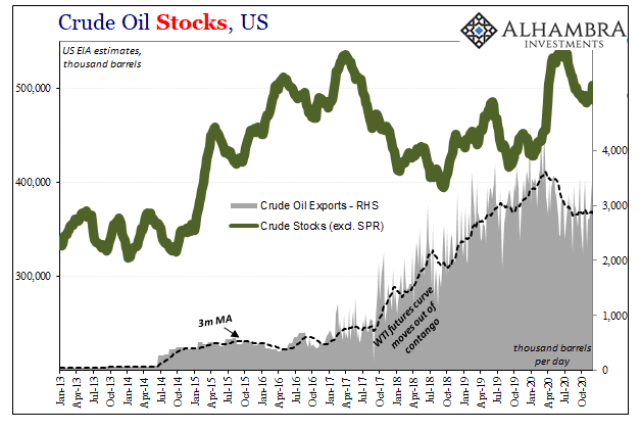

What’s Going On, And Why Late August?29 Oct 2020

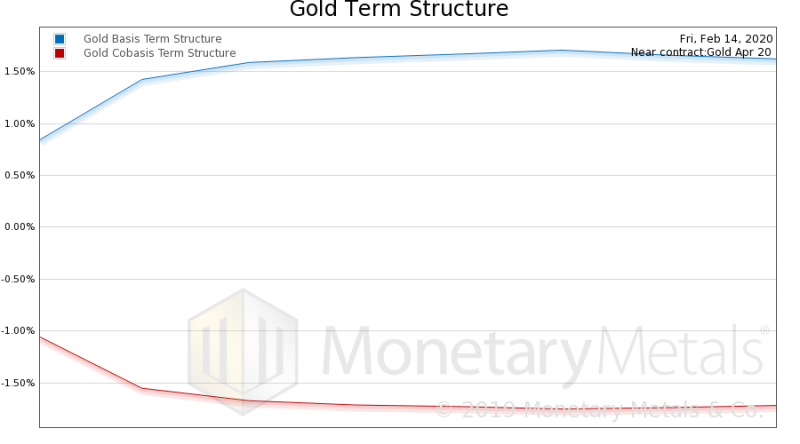

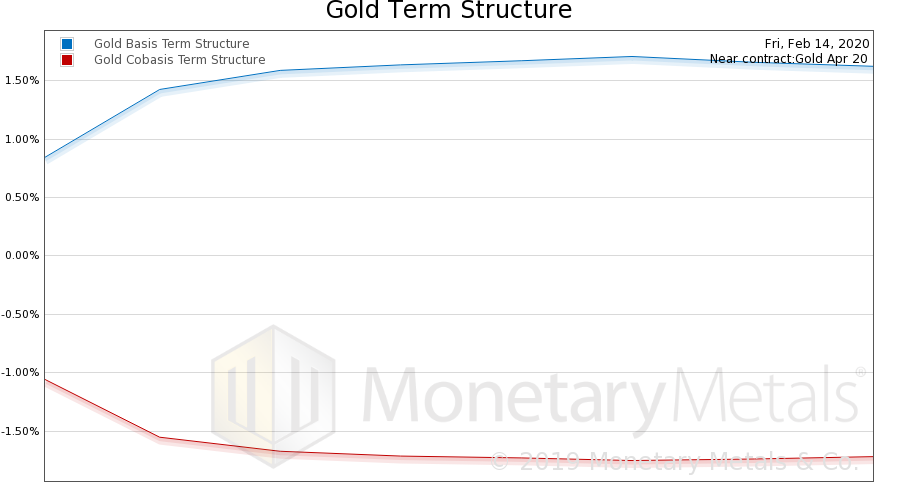

Widening Bid-Ask Spreads, Gold and Silver Market Report 17 February

Widening Bid-Ask Spreads, Gold and Silver Market Report 17 February17 Feb 2020

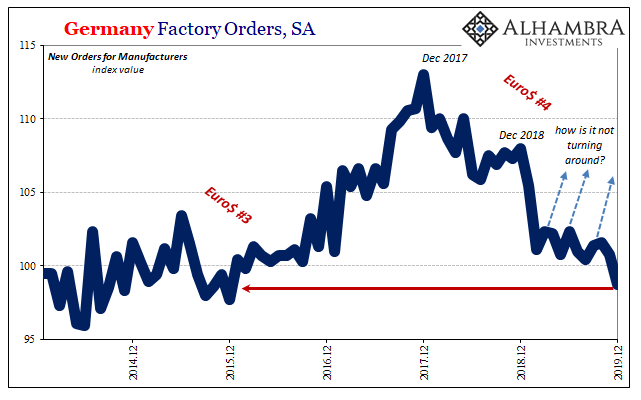

COT Black: German Factories, Oklahoma Tank Farms, And FRBNY9 Feb 2020

Tidbits Of Further Warnings: Houston, We (Still) Have A (Repo) Problem18 Oct 2019

Nothing To See Here, It’s Just Everything4 Jan 2019

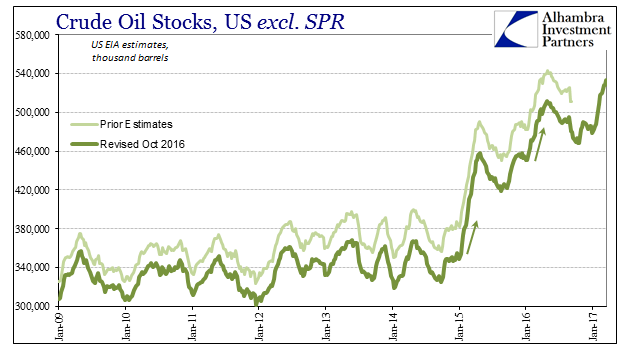

Economics Through The Economics of Oil23 Mar 2017