Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

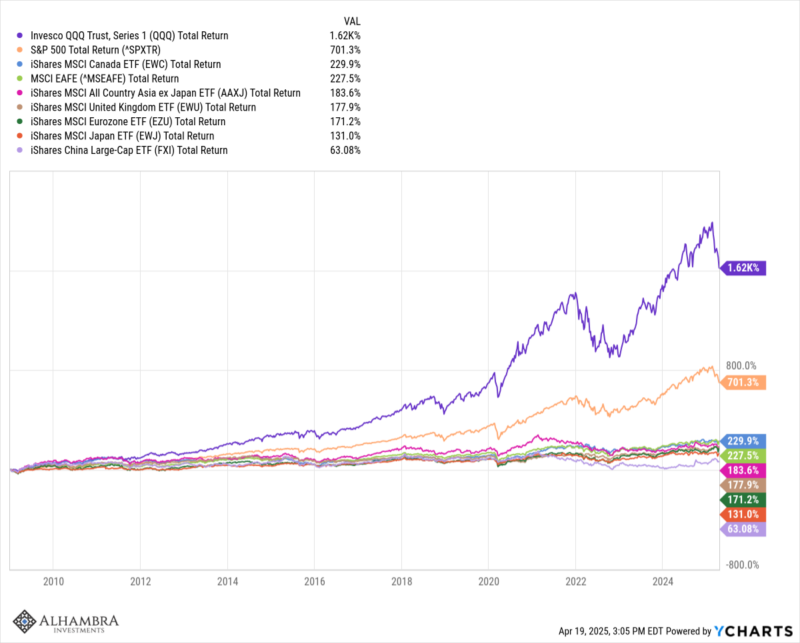

Weekly Market Pulse: Peak America?

Weekly Market Pulse: Peak America?21 Apr 2025

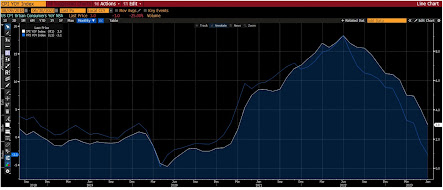

Ueda Lifts Yen, Leaving Euro and Sterling Pinned Near Lows

Ueda Lifts Yen, Leaving Euro and Sterling Pinned Near Lows21 Nov 2024

Higher Yields Help Extend the Dollar’s Gains12 Nov 2024

The ECB and the $1.10 level in the Euro12 Sep 2024

Disappointing US Data Followed by Better Japanese Wages and Stronger German Factory Orders Weigh on the Greenback5 Sep 2024

Dollar Comes Back Bid13 Jun 2024

Dollar Pulled Back in Europe. New Buying Opportunity?30 May 2024

Quiet End to a Busy Week16 Feb 2024

Food Prices Drive China’s CPI Lower while the Greenback is Mostly Firmer in Narrow Ranges9 Nov 2023

BRICS to Expand a Little, USD Steadies after Yesterday’s Retreat, Attention Turns to Jackson Hole24 Aug 2023

Aussie Recovers from Poor Jobs Data, but Nokkie is Weaker Despite Rate Hike17 Aug 2023

The Greenback is Softer Ahead of CPI but Key Chart Points Remain Intact10 Aug 2023

RBNZ Delivers a Dovish Hike and UK Inflation Surprises to the Upside24 May 2023

Equities Retreat while the Dollar is Confined to Narrow Ranges20 Apr 2023

Dollar Soft but Stretched30 Mar 2023

Firmer Rates and Higher Bank Stocks Give the Greenback Little Help28 Mar 2023

Higher for Longer Helps the Dollar while Weighs on Equities2 Mar 2023

Ueda Day24 Feb 2023

US Interest Rate Adjustment Post-Jobs is Over as the 2-Year Yield Backs Away from 4.50%9 Feb 2023

Sharp Dollar Setback may offer Bulls a Bargain9 Sep 2022