Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Update The Conflict of Interest Rate(s)

Update The Conflict of Interest Rate(s)13 Jun 2022

Did Central Banks arrive at their Target Inflation Rate by Mere Fluke?

Did Central Banks arrive at their Target Inflation Rate by Mere Fluke?26 May 2022

What Really ‘Raises’ The Rising ‘Dollar’3 May 2022

We Can Only Hope For Another (bond) Massacre30 Mar 2022

Another One Inverts, The Retching Cat Reaches Treasuries15 Mar 2022

The ‘Fed Put’ – Gone Until There’s Blood in the Streets

The ‘Fed Put’ – Gone Until There’s Blood in the Streets30 Jan 2022

Taper Discretion Means Not Loving Payrolls Anymore10 Jan 2022

One Shock Case For ‘Irrational Exuberance’ Reaching A Quarter-Century22 Dec 2021

Consumers, Too; (Un)Confident To Re-engage19 Dec 2020

Fama 2: No Inflation For Old Central Banks14 Aug 2020

The Greenspan Moon Cult5 Mar 2020

History Shows You Should Infer Nothing From Powell’s Pause2 Feb 2020

More (Badly Needed) Curve Comparisons23 Nov 2019

More Than A Decade Too Late: FRBNY Now Wants To Know, Where Were The Dealers?24 Sep 2019

Big Difference Which Kind of Hedge It Truly Is3 Sep 2019

As Chinese Factory Deflation Sets In, A ‘Dovish’ Powell Leans on ‘Uncertainty’14 Jul 2019

Proposed Negative Rates Really Expose The Bond Market’s Appreciation For What Is Nothing More Than Magic Number Theory23 May 2019

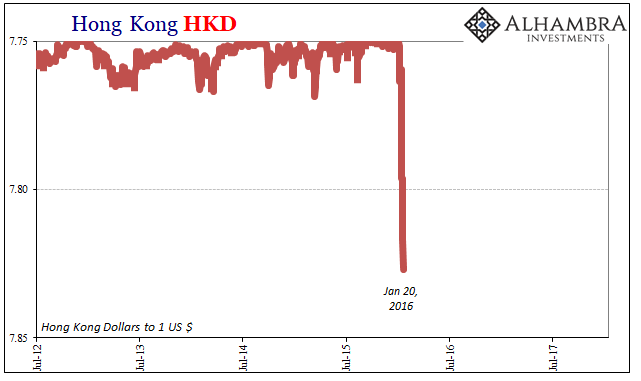

Central Bank Transparency, Or Doing Deliberate Dollar Deals With The Devil25 Jan 2018

If Bitcoin Is A Bubble…7 Jan 2018

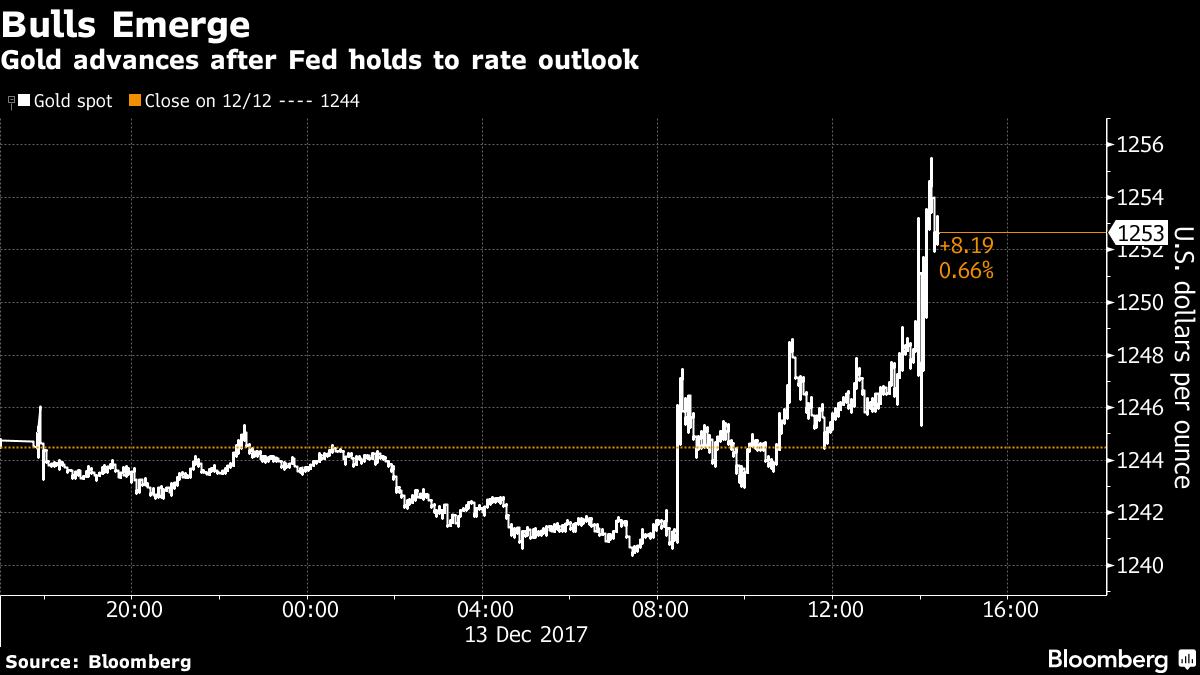

Year-end Rate Hike Once Again Proves To Be Launchpad For Gold Price

Year-end Rate Hike Once Again Proves To Be Launchpad For Gold Price15 Dec 2017

Did Central Banks arrive at their Target Inflation Rate by Mere Fluke?

2022-05-26

by Stephen Flood

2022-05-26

Read More »