BALTIMORE – On Tuesday, the Dow sold off – down 133 points. Oil traded in the $36 range. And Donald J. Trump lost the Wisconsin primary to Ted Cruz. Overall, world stocks have held up well, despite cascading evidence of impending doom.

With higher rates, Yellen risks corporate profits and bond defaults

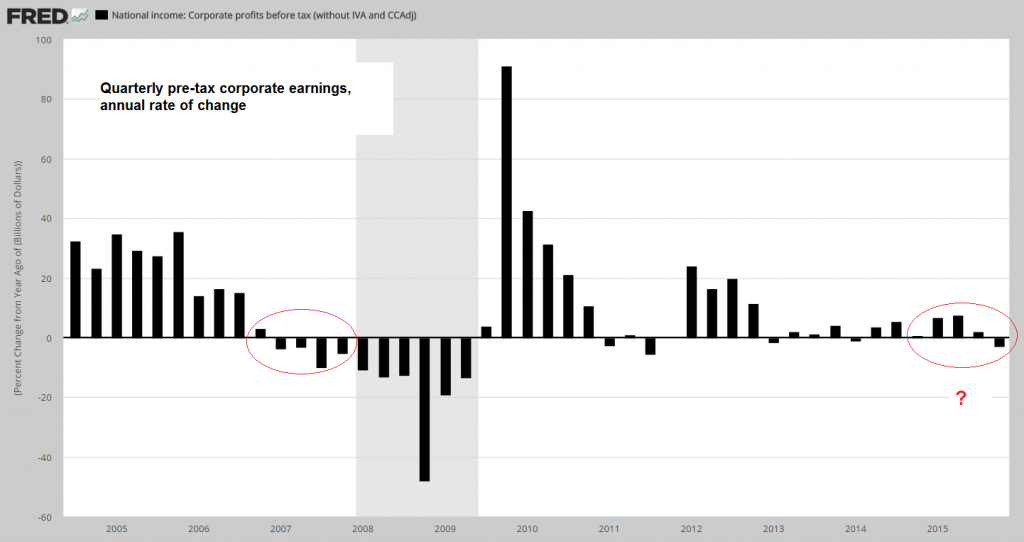

U.S. corporate profits have been in decline since the second quarter of 2015. Globally, 36 corporate bond issues have defaulted so far this year – up from 25 during the same period of 2015. Economists at JPMorgan Chase put the U.S. economy growth rate for the first quarter at 0.7% – down by over one-third from earlier estimates.

| With higher rates, Yellen risks corporate profits and bond defaults

Annual rate of change in quarterly pre-tax profits: |

Bill Bonner explains why the Fed will normalize interest rates. With higher rates, Yellen risks corporate profits and bond defaults. With higher rates, Yellen risks not only bond defaults, but also bank defaults. - Click to enlarge |

With higher rates, Yellen risks not only bond defaults, but also bank defaults

And there is $1.7 trillion in junk bonds outstanding – a trillion more than in 2008. Some of these are sure to default in the months ahead. Speculators are already shorting the banks with the biggest piles of these grenades in their vaults.

Over the last few days, we’ve been trying to coax out an insight. It concerns whether Fed chief Janet Yellen really does have investors’ backs. Not that we have any doubt about her intentions.

Her career has been financed and nurtured by credit and the people who provide it. Crony capitalists, corrupt politicians, and Deep State hustlers paid good money for her; she’ll do all she can to avoid letting them down.

| With higher rates, Yellen risks not only bond defaults, but also bank defaults

Bank stocks vs. the S&P 500 Index Bank stocks vs. the S&P 500 Index: |

Bill Bonner explains why the Fed will normalize interest rates. With higher rates, Yellen risks corporate profits and bond defaults. With higher rates, Yellen risks not only bond defaults, but also bank defaults. - Click to enlarge |

But something isn’t working. Not for her. Not for Bank of Japan governor Haruhiko Kuroda. Not for the president of the European Central Bank, Mario Draghi. Not for People’s Bank of China governor Zhou Xiaochuan. Their tricks no longer work.

The Fed will NEVER normalize interest rates

We’re on record with a bold prediction: The Fed will NEVER normalize interest rates. Readers may wonder how that jives with our deeper insight: Nobody knows anything. And of course, we don’t know whether the Fed will normalize or not. But let us further explain our reasoning; you make up your own mind as to where to place your bet.

| They’ve built a big house of cards and they presumably realize it by now (how can they not?) |

|

Consumers are in better shape, but governments and corporations are in worse shape

The short version of our argument: For the last eight years, the Fed has tried to stimulate the economy with ultra-low interest rates. Business, consumers, and government now almost all depend on credit… and most need ultra-low rates to make ends meet.

Consumers are in better shape, generally, than they were in 2008. But corporations and governments are in worse shape. Raise the cost of funding, and you will push many of them over the edge.

Banks, pension funds, and insurance companies are especially vulnerable. They’re now stocked up with low-yield government bonds. Should interest rates rise, those bonds will go down in price. In other words, raising rates will provoke the very calamity the Fed was trying to avoid: the bankruptcy of the financial sector.

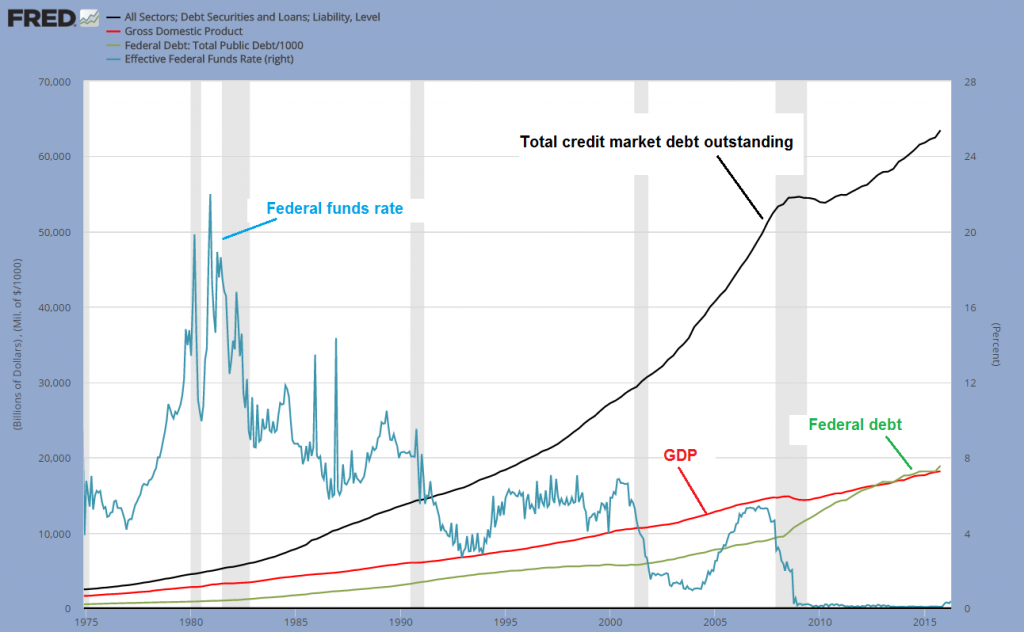

The Ever-Rising Debt

But wait…how did Bernanke, Yellen, Kuroda, Draghi et al. think they would ever get away with it? How could they believe – even for a minute – that a debt problem could be solved by adding more debt? And yet, they always got away with it before.

After World War II, for example, the feds had a higher debt-to-GDP ratio than they have now. But after the war, the economy boomed, inflation rose… and soon the debt was no problem. Again, at the beginning of President’s Reagan’s first term, economists worried about large government deficits.

| The ever-rising debt: The “there’s no coming back from this” chart:

total US credit market debt (black line), |

|

Why the Reagan Revolution Failed

The job of colleague David Stockman – director of Reagan’s budget team – was to bring those deficits under control. He failed… a story well told in his book The Triumph of Politics: Why the Reagan Revolution Failed.

Conservative economists thought the U.S. would sink into another slimy pool of deficits and debt. But once again, a spurt of growth (with low deficits) during the Clinton years reduced the debt to a more manageable level. So, why worry?

Because this time, it’s not working. Growth is slowing. Productivity has stalled. As former Goldman boy Gavyn Davies put it in the Financial Times: “The slowdown in labor productivity accounts for most of the massive disappointment in global output growth since just before the 2008 crash.”

Professor Robert Gordon at Northwestern University believes there is more to it than just a cyclical downturn. He maintains that the extraordinary growth of the Industrial Revolution had played itself out by the 1980s. And it can’t be repeated.

We have another hypothesis (which we’ll talk more about tomorrow): Either way, the debt can never, voluntarily, be brought under control. And the Fed can never “normalize” rates. More to come…

Charts by St. Louis Federal Reserve Research, StockCharts

Chart and image captions by PT

The above article originally appeared at the Diary of a Rogue Economist, written for Bonner & Partners. Bill Bonner founded Agora, Inc in 1978. It has since grown into one of the largest independent newsletter publishing companies in the world. He has also written three New York Times bestselling books, Financial Reckoning Day, Empire of Debt and Mobs, Messiahs and Markets.