Does any of this make sense? No. But it’s so darn profitable to the oligarchy, it’s difficult to escape debt-serfdom and tax-donkey servitude.

We rarely ask “does this make any sense?” of things that are widely accepted as beneficial – or if not beneficial, “the way it is,” i.e. it can’t be changed by non-elite (i.e. the bottom 99.5%) efforts.

Of the vast array of things that don’t make sense, let’s start with borrowing from future income to spend more today. This is of course the entire foundation of consumer economies such as the U.S.: the number of households which buy a car or house with cash is near-zero, unless 1) they just sold a bubble-valuation house and paid off their mortgage in escrow or 2) they earned wealth via fiscal prudence, i.e. the avoidance of debt and the exultation of saving.

Debt has this peculiar characteristic: it has to be paid back with interest.Depending on the rate of interest and the length of the loan, this translates into a mind-numbing reality: borrowing $100 can cost $200 once interest is factored in.

One might reckon that people would be cautious about paying two or three times more for something by using debt rather than cash. But consumer economies are based not just on debt, but on TINA (there is no alternative) and on the timeless seduction of getting something now and paying for it later.

College students are frightened by scary stories of permanent impoverishment and social degradation if they don’t borrow a small fortune to buy a diploma (never mind if you actually learn anything remotely useful or wise; you’re not buying an education, you’re buying an accreditation of your ability to grind through a bureaucratic system without any unhealthy questioning if “higher education” actually makes any sense. Hint: it doesn’t, unless you’re skimming wealth off the poor students.)

The higher education debt scam is classic TINA: there is no alternative to borrowing a small fortune to buy a (mostly worthless) diploma, unless you favor living in a cardboard box the rest of your life.

TINA drives the trillion-dollar deficits of the US government as well: the entrenched self-serving interests feeding at the public trough would quickly ramp the political pain to 11 if their share suffered any cuts, and so There Is No Alternative to funding every parasitic, predatory cartel with its maw in the public trough (healthcare, higher education, banking, national defense, etc.)

Tragically, for a lot of low-income working poor households, there really isn’t any alternative to high-interest debt. When the tire on the gets-me-to-work vehicle blows, the expense has to be financed, either at the tire shop or with a credit card.

Equally tragically, fiscal prudence, i.e. the avoidance of debt and the exultation of saving, is not taught in our educational system. As those of us who work in construction know, many blue-collar tradescraft folks earn good pay, but they mis-spend it on needless consumption or over-borrow to buy stuff they could easily live without.

I could list dozens of personal histories of earned wealth squandered on painfully frivolous consumption or “investments” that never seem to actually increase the owner’s wealth.

What’s not taught in our educational system–perhaps because it would undermine Consumption Funded by Debt?) –is opportunity cost: when you buy the $100 item and end up paying $200 or $300 because the purchase was funded by debt, the opportunity cost is: what else could you have done with the money squandered on interest, penalties, late fees etc.?

This opportunity cost separates those with decent earnings and little productive wealth and those who earned the same income but acquired real wealth. The flip side of debt (paying interest) is earning interest on savings/ capital. Those with capital can earn a return on their capital while those with only debt are debt-serfs, devoting much of their future earnings to the repayment of debt with interest. (Late fees and other charges can triple the cost of the initial purchase in short order.)

Pre-easy-credit, people couldn’t borrow money for the simple reason they were poor credit risks. Credit has always existed, but it was generally linked to collateral and / or a transaction that would soon settle the debt in cash, for example, a loan extended by a wholesaler who will get paid off once the end-customer pays.

With public debt, the collateral is the tax-donkey’s obligation to pay taxes, and with private-sector debt, the borrower’s future income. If the tax-donkey closes down his/her business and sells his/her house, the obligation to pay taxes vanishes into thin air (after the tax-donkey pays the transfer taxes, of course, and any capital gains on the sale of the house.)

| The debtor who has no collateral other than his/her future income has a trick card to play: bankruptcy. Since there’s no real-world asset for the lender to repossess (or in the case of used cars, the repo’d vehicle is typically worth less than the outstanding loan), the borrower can stiff the lender.

But since the lenders own the political machinery, bankruptcy will cost you. In the case of student loan debt, it’s not easy to get out from underneath student loan debt. In the case of credit card debt default, the lenders will cut the defaulted borrower off from access to credit: it’s cold turkey withdrawal from credit, Baby. TINA no longer matters; there’s no credit available except from loan sharks, and their rates guarantee poverty (or very unfortunate “accidents”.)

Does any of this make sense? No. But it’s so darn profitable to the oligarchy, it’s difficult to escape debt-serfdom and tax-donkey servitude. Interestingly, when there really is no alternative, people tend to get creative / innovative. But when easy credit is available, they default to taking the easy way out, which is to borrow from future earnings without questioning the opportunity cost of debt-serfdom and tax-donkey servitude.

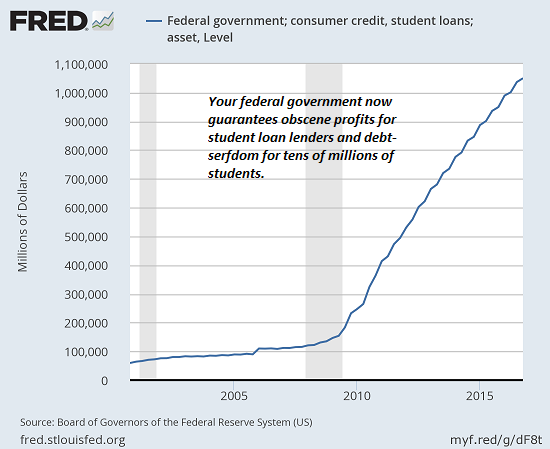

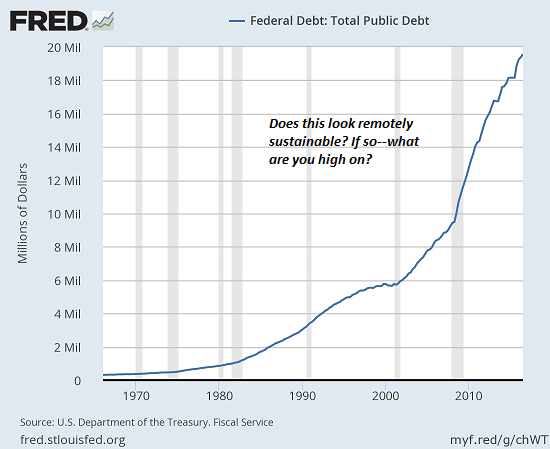

Remember: every dollar of debt is an expense to the borrower but a source of income to the lender. Keep that in mind as you study these charts of student loan debt and federal debt: |

Federal Government; Student loans 2005-2018 - Click to enlarge |

| Future income devoted to paying interest is money that can’t be invested productively. On a national scale, that guarantees falling productivity, soaring wealth inequality and eventually, widespread impoverishment. |

US Federal Debt 1970-2018 - Click to enlarge |

Full story here

Are you the author?

At readers' request, I've prepared a biography. I am not confident this is the right length or has the desired information; the whole project veers uncomfortably close to PR. On the other hand, who wants to read a boring bio? I am reminded of the "Peanuts" comic character Lucy, who once issued this terse biographical summary: "A man was born, he lived, he died." All undoubtedly true, but somewhat lacking in narrative.

Previous post

See more for 5.) Charles Hugh Smith

Next post

Tags:

newsletter