Latest Investment OutlookIn his latest investment outlook, Fasanara Capital’s Franceso Filia, who two months ago explained in one chart how the “fake market” operates… … discuss what happens when a “Twin Bubble meets quantitative tightening” and answers why record-low volatility breeds market fragility and precedes system instability. We’ll have more to share on that shortly, but for now, here is Filia with his take on ‘when do we know these are delusional markets‘:

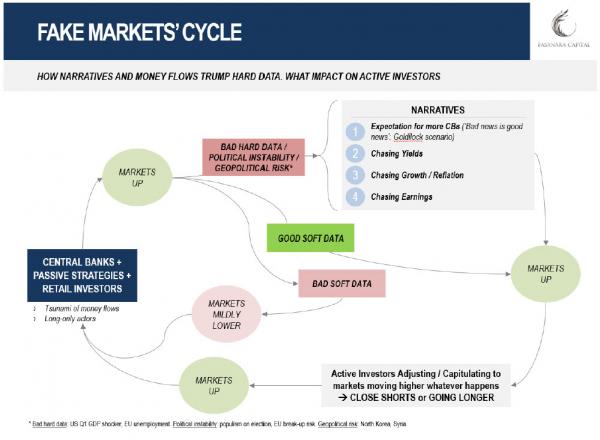

|

Markets Cycle - Click to enlarge |

| Cov-Lite Loans In Both EU And The US Reached A Staggering 70% Of All Loan Supply In 2017. Before the credit bubble burst in 2007, it was 30%. |

European Leveraged Loan Issuance, 2006 - 2017 - Click to enlarge |

ZeroHedges' Tyler Durden is the hero of Fight Club, the 1999 movie based on Chuck Palahniuk's novel that reflected Chuck's experience in the Cacophony Society Quote: "Goddamn it, an entire generation pumping gas, waiting tables, slaves with white collars. Advertising has us chasing cars and clothes, working jobs we hate so we can buy shit we don’t need. We’re the middle children of history, man. No purpose or place. We have no Great War. No Great Depression. Our Great War’s a spiritual war… our Great Depression is our lives. We’ve all been raised on television to believe that one day we’d all be millionaires, and movie gods, and rock stars. But we won’t. And we’re slowly learning that fact. And we’re very, very pissed off." --> see more about Tyler on snbchf

Tags: Bank of Japan,Bond,Business,Economic bubble,economy,Equity Markets,European central bank,European Union,Japan,Loans,newslettersent,Private Equity,SP,Swiss National Bank,Volatility