Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

For five years, governance reforms at the IMF have been stymied by the refusal of the US Congress to accept a new and higher quota (money) to the IMF. This has frustrated efforts to integrate the developing countries, especially the large ones, like China, better into the global economy. It may have also helped spur China to develop parallel organizations, like the Asian Infrastructure Investment Bank.

The omnibus spending and tax bill that looks likely to be approved by Congress and signed by Obama in the coming days includes a provision to accept the IMF reforms.

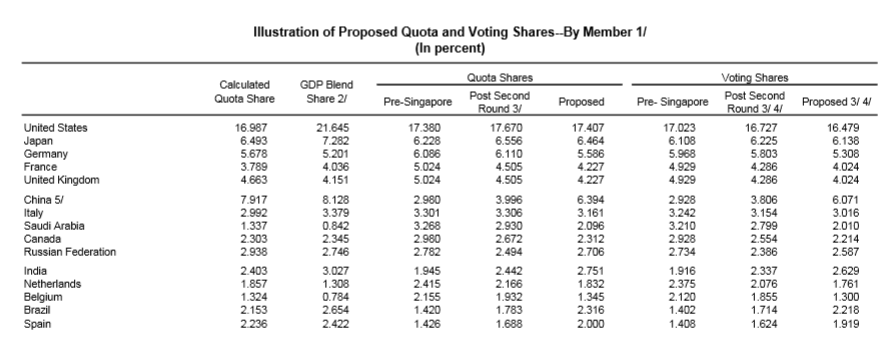

When the reforms are enacted, the US weighted voting authority will slip to 16.5% from 16.7%. As many decisions require an 85% majority, the US retains its effective veto. China's voting weight reportedly would rise from 3.8% to 6.0%. As was the case with the SDR decision, the rise of China comes at the expense of Europe, not the US.

In exchange for its approval, Congress is demanding a greater role in some IMF decisions. Specifically, the agreement reportedly will require the Administration to work toward repealing the "systemic exception" created in 2010 to allow the IMF to take part in European aid to Greece. The extent of the IMF's involvement in Europe has troubled many members, including the US apparently.

The legislation also would require that the Administration notifies Congress at least a week before an IMF vote is held on "exceptional access". This is the practice by which the IMF can lends funds above normal limits on a case-by-case basis. It requires the approval of the Fund’s Executive Board. Congress is also insisting that a study be launched to see if collateral should be required for such loans.

These seem like relatively minor encroachments by the US Congress. The more important consideration is that it begins the long overdue process of modernizing the IMF. Begins in the operative word because this is only a first and modest step. The reforms will double the IMF's quotas and shift six percent of the quota shares to emerging and developing countries. About half the shift comes from developed countries, mostly Europe, and a third from the oil producers. The high income countries in Europe will have two few seats on the Executive Board, and will be replaced by two directors from lower income countries. Projections indicate that about 110 of the 187 IMF members will see their quota shares increased or maintained.

Here is a table from the IMF that illustrates the proposed changes for the top fifteen members. The footnote on China refers to the fact that China include Hong Kong and Macau.

One issue that is on few people's radar screens is that Lagarde's term as Managing Director of the IMF ends in July 2016. There had been some speculation that she would enter French politics, where the presidential election will be held in 2017. However, she has indicated a willingness to serve a second terms at the IMF's helm. Lagarde is an adroit politician, and has tried to protect her flanks, but the criticism of the IMF's large exposure to Europe does not set well with many.

Arguably more importantly, the European domination of the head of the IMF continues to be questioned. India's Rajan or Mexico's Carstens are thought to be potential rival candidates. However, the challenge is that the emerging and developing countries struggle to unite behind a single candidate, which fragments their voice.

Meanwhile the IMF has yet to decide whether it will participate in the third assistance package that was launched this past summer. Ironically, some German officials that opposed IMF involvement at the beginning of the crisis now insist on it. However, the IMF is demanding greater debt relief that many of the creditors seem to be willing to accept. Although the EU heads of state summit begins today, immigration/refugees and the related frontier issues will likely dominate the agenda. A decision also may be made on extending the sanctions on Russia that are set to expire at the end of next month. Debt relief for Greece and the UK's reform demands may be discussed on the margins will likely be more salient early next year.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: