Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Simple Economics and Money Math

Simple Economics and Money Math12 Jun 2022

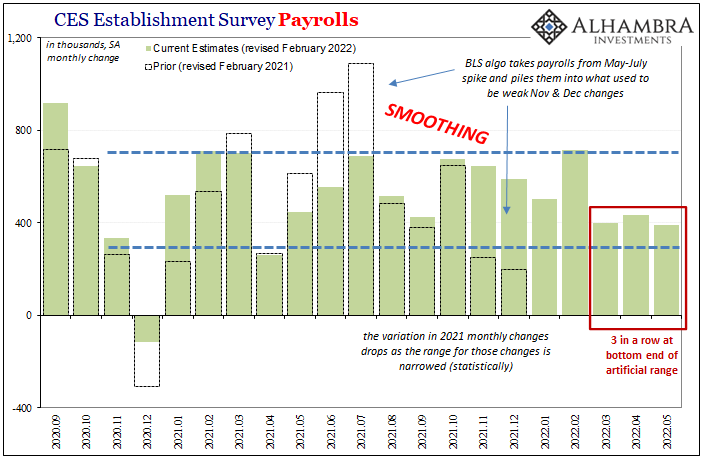

May Payrolls (and more) Confirm Slowdown (and more)7 Jun 2022

ADP Front-Runs BLS and President Phillips4 Jun 2022

For The Fed, None Of These Details Will Matter6 Mar 2022

Taper Discretion Means Not Loving Payrolls Anymore10 Jan 2022

How Many More Americans Might Have Quit Their Jobs Than The Huge Number Already Estimated, And What Might This Mean For FOMC Taper7 Jan 2022

As The Fed Tapers: What If More Rapid (published) Wage Increases Are Actually Evidence of *Deflationary* Conditions?5 Jan 2022

A Global JOLT(s) In July9 Dec 2021

The Productive Use Of Awful Q3 Productivity Estimates Highlights Even More ‘Growth Scare’ Potential8 Dec 2021

The Wile E. Powell Inflation: Are We Really Just Going To Ignore The Cliff?6 Nov 2021

Isn’t the Labor Shortage Transitory?5 Nov 2021

Weekly Market Pulse: Perception vs Reality

Weekly Market Pulse: Perception vs Reality18 Oct 2021

For The Love Of Unemployment Rates12 Oct 2021

Weekly Market Pulse: Zooming Out3 Oct 2021

An Economy Dividing By Inventory And Labor30 Sep 2021

Do Rising ‘Global’ Growth Concerns Include An Already *Slowing* US Economy?23 Jul 2021

JOLTS Revisions: Much Better Reopening, But Why Didn’t It Last?12 Mar 2021

Weekly Market Pulse – Real Rates Finally Make A Move

Weekly Market Pulse – Real Rates Finally Make A Move22 Feb 2021

Two Seemingly Opposite Ends Of The Inflation Debate Come Together19 Feb 2021

Uncle Sam Was Back Having Consumers’ Backs18 Feb 2021