Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Fragile and Consolidative Tone Starts the Week in FX

Fragile and Consolidative Tone Starts the Week in FX18 Nov 2024

Dollar Storms Back (but not Against the Yen) After Fed Signals Low Bar to September Cut1 Aug 2024

Yen’s Surge Continues, while PBOC Surprises with Another Rate Cut, and US 2-30 Year Yield Curve Ends Inversion25 Jul 2024

BOJ Appears to have Intervened last Friday Too, but Market Sells Yen Anyway16 Jul 2024

Market Takes JPY Lower Despite Intervention Speculation, While Sterling Shines12 Jul 2024

May Day Fed Day1 May 2024

Yen Retreats, while Stronger EMU GDP Underscores Nascent Recovery and Lifts the Euro30 Apr 2024

China PMI is Better than Expected but the Greenback Still Rises above CNY7.231 Apr 2024

Waller Pushes on Open Door: Push for Patience Lifts the Dollar, Complicating Japanese Efforts28 Mar 2024

CNY7.20 Gives Way as Strong Greenback Proves Too Much22 Mar 2024

Calm Start to the Week, with Little Impact from Russia’s Drama

Calm Start to the Week, with Little Impact from Russia’s Drama26 Jun 2023

It is not So Much about the Fed’s hike Today but the Forward Guidance

It is not So Much about the Fed’s hike Today but the Forward Guidance2 Nov 2022

Sterling and UK Debt Market Respond Favorably to the Return of Orthodoxy17 Oct 2022

Week Ahead: Focus Shifts away from the US after Robust Jobs Data and Stronger than Expected Inflation

Week Ahead: Focus Shifts away from the US after Robust Jobs Data and Stronger than Expected Inflation15 Oct 2022

Can We Look Past US CPI ?13 Oct 2022

Intraday Momentum Indicators Point to a Dollar Recovery After the Employment Report7 Oct 2022

Markets Remain on Edge14 Sep 2022

Will the Dollar Recover After CPI?13 Sep 2022

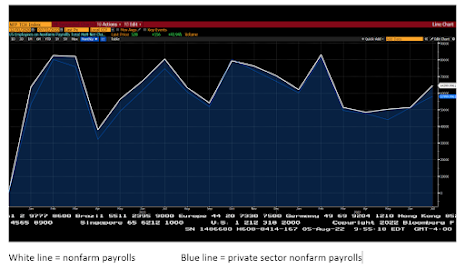

Dog Days8 Aug 2022

Johnson’s Ability to Lead Tories into Victory at Risk with Today’s By-Elections23 Jun 2022