Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Banks Or (euro)Dollars? That Is The (only) Question

Banks Or (euro)Dollars? That Is The (only) Question3 Apr 2020

Tidbits Of Further Warnings: Houston, We (Still) Have A (Repo) Problem18 Oct 2019

Head Faking In The Empty Zoo: Powell Expands The Balance Sheet (Again)9 Oct 2019

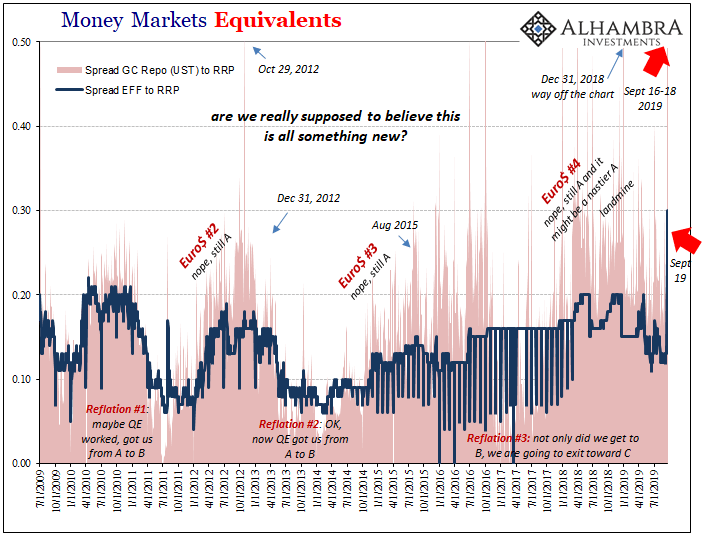

What’s The Verdict On This Week?21 Sep 2019

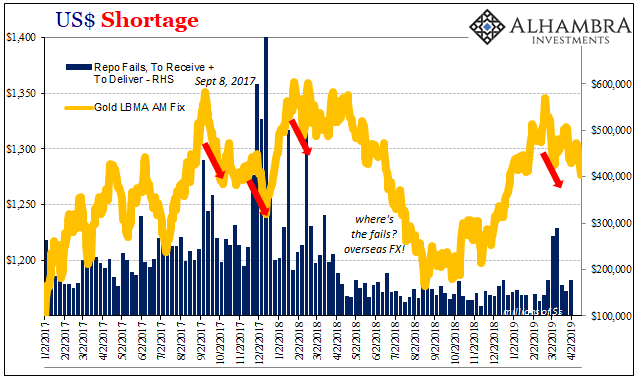

COT Blue: Distinct Lack of Green But A Lot That’s Gold24 Apr 2019

Phugoid Dollar Funding4 Apr 2019

The Real End of the Bond Market

The Real End of the Bond Market22 Mar 2019

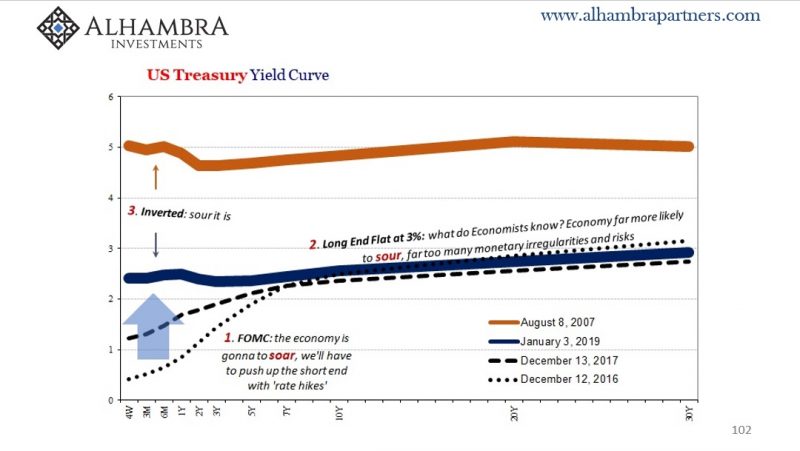

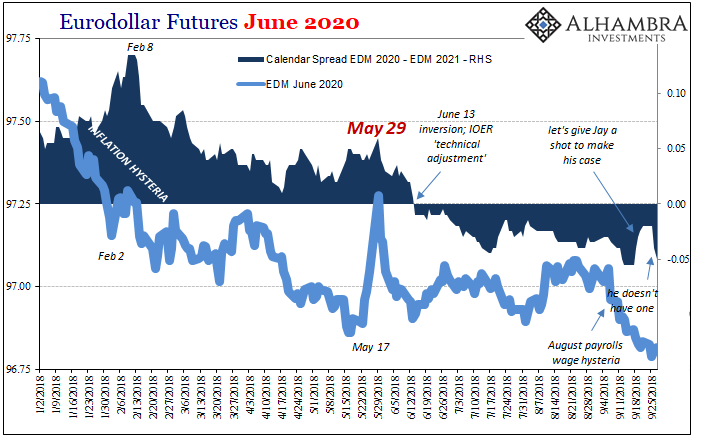

Make Your Case, Jay28 Sep 2018

Anticipating How Welcome This Second Deluge Will Be29 Aug 2018