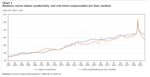

Originally published by Law&Liberty. The Consumer Financial Protection Bureau (CFPB) has been a source of controversy since its creation. Critics of the agency have long argued that its independent status is unconstitutional. In a recent decision, however, the Supreme Court affirmed the constitutionality of the CFPB’s funding scheme, even though it circumvents the normal Congressional appropriation process by “allowing the Bureau to draw money from the earnings of the Federal Reserve System.”This decision belies the Fed’s current financial condition and conflicts with provisions in the Federal Reserve Act. The fact of the matter is that the Fed no longer has any earnings. It currently has huge cash operating losses and must borrow to fund both the Fed’s and the CFPB’s operations. When it

Read More »2024-06-07