Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

Gold Buying Ramps Up Globally, but Silver Could Get Interesting

Gold Buying Ramps Up Globally, but Silver Could Get Interesting19 Apr 2024

Boost Your Savings: Strategies for the Accumulation and Distribution Phases

Boost Your Savings: Strategies for the Accumulation and Distribution Phases19 Apr 2024

4-19-24 Did You Pay Your Fair Share of Taxes?

4-19-24 Did You Pay Your Fair Share of Taxes?19 Apr 2024

Navigating Market Bubbles and Lessons on Shorts – Andy Tanner

Navigating Market Bubbles and Lessons on Shorts – Andy Tanner18 Apr 2024

How the World can Tackle Climate Change

How the World can Tackle Climate Change18 Apr 2024

Is The Gold Price Too High To Buy? The Train Hasn’t Left The Station!

Is The Gold Price Too High To Buy? The Train Hasn’t Left The Station!18 Apr 2024

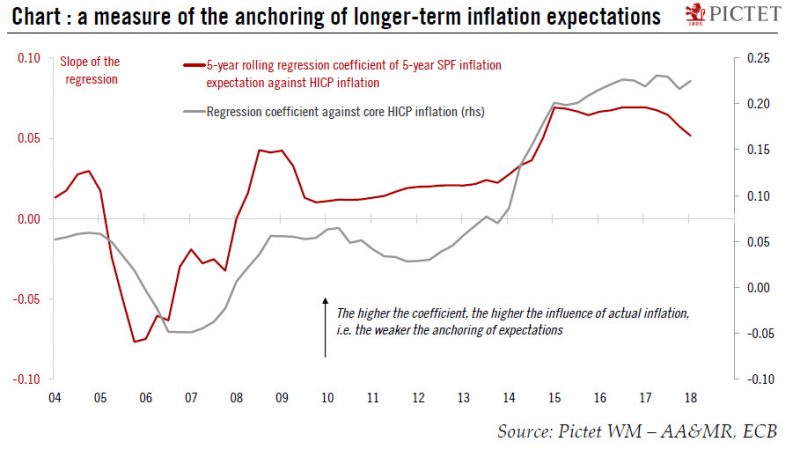

Understanding the Recent Inflation Spike and the Federal Reserve’s Reaction

Understanding the Recent Inflation Spike and the Federal Reserve’s Reaction18 Apr 2024

Mit dem Flugzeug pendeln, um Miete zu sparen? ️ #pendeln

Mit dem Flugzeug pendeln, um Miete zu sparen? ️ #pendeln18 Apr 2024

Mein YouTube Einnahmen: Totale Transparenz

Mein YouTube Einnahmen: Totale Transparenz18 Apr 2024

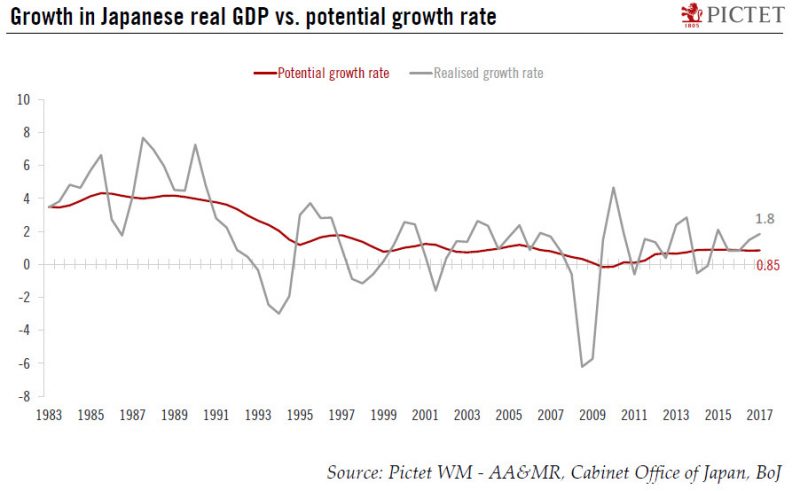

4-18-24 Are We On Japan’s Path to Stagnation?

4-18-24 Are We On Japan’s Path to Stagnation?18 Apr 2024

Eilt: dramatische Wende im Ukraine-Konflikt!

Eilt: dramatische Wende im Ukraine-Konflikt!18 Apr 2024

Widerstand zwecklos (?): DJE-plusNews April 2024 mit Mario Künzel und Moritz Rehmann

Widerstand zwecklos (?): DJE-plusNews April 2024 mit Mario Künzel und Moritz Rehmann18 Apr 2024

Gold Technical Analysis – Where will we break out to?

Gold Technical Analysis – Where will we break out to?18 Apr 2024

Baerbock vermasselt Tagesthemen Interview komplett!

Baerbock vermasselt Tagesthemen Interview komplett!18 Apr 2024

Wichtige Morning News mit Oliver Klemm #284

Wichtige Morning News mit Oliver Klemm #28418 Apr 2024

Wichtige Morning News mit Oliver Klemm #285

Wichtige Morning News mit Oliver Klemm #28518 Apr 2024

ECBs Lagarde says exchange rates matter and it leads to a rotation higher

ECBs Lagarde says exchange rates matter and it leads to a rotation higher17 Apr 2024

Financial Trends for 2024: Banks, Bitcoin, and Real Estate – Robert Kiyosaki, Gerald Celente

Financial Trends for 2024: Banks, Bitcoin, and Real Estate – Robert Kiyosaki, Gerald Celente17 Apr 2024

Climate Change Efforts Must Be Practical and the Time is NOW

Climate Change Efforts Must Be Practical and the Time is NOW17 Apr 2024

Mir bleibt die Spucke weg! Desolates Stern Interview von SPD Ministerin!

Mir bleibt die Spucke weg! Desolates Stern Interview von SPD Ministerin!17 Apr 2024