Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

SNB Losses in the News

SNB Losses in the News1 Aug 2022

The SNB’s Financial Result, Currency Reserves, and Distribution Reserve

The SNB’s Financial Result, Currency Reserves, and Distribution Reserve27 Jul 2022

“Digitales Notenbankgeld – und nun? (CBDC—What Next?),” FuW, 2021

“Digitales Notenbankgeld – und nun? (CBDC—What Next?),” FuW, 20218 Dec 2021

“Die Nationalbank ist an vielen Fronten gefordert (Challenges for the Swiss National Bank),” NZZ, 2021

“Die Nationalbank ist an vielen Fronten gefordert (Challenges for the Swiss National Bank),” NZZ, 202110 Aug 2021

West Virginia Gov. Personally On The Hook For $700MM In Greensill Collapse

West Virginia Gov. Personally On The Hook For $700MM In Greensill Collapse1 Jun 2021

“Everything Is On Fire”

“Everything Is On Fire”20 May 2021

UBS Reportedly Re-Starts Layoffs After “Doubling” One Time Bonuses To Some Associates

UBS Reportedly Re-Starts Layoffs After “Doubling” One Time Bonuses To Some Associates12 May 2021

UBS, Desperate To Retain Talent, Now Offering $40,000 Bonuses To Newly Promoted Associates

UBS, Desperate To Retain Talent, Now Offering $40,000 Bonuses To Newly Promoted Associates11 May 2021

Credit Suisse Hires Former Prime Brokerage Head To Restore Business After Archegos Blowup

Credit Suisse Hires Former Prime Brokerage Head To Restore Business After Archegos Blowup9 May 2021

Gold Is Laughing At Powell

Gold Is Laughing At Powell3 May 2021

The $3 Trillion Hidden Exposure Behind The Archegos Blowup

The $3 Trillion Hidden Exposure Behind The Archegos Blowup2 May 2021

“Die Schattenseiten von Schuldenbremsen (The Dark Side of Debt Limits),” ifoSD, 2021

“Die Schattenseiten von Schuldenbremsen (The Dark Side of Debt Limits),” ifoSD, 202116 Apr 2021

Credit Suisse Dumping Huge Archegos Blocks; Liquidating Millions In VIACS, VIPS And FTCH

Credit Suisse Dumping Huge Archegos Blocks; Liquidating Millions In VIACS, VIPS And FTCH6 Apr 2021

Gold Could Offer A Way Out Of Switzerland’s Failing Inflationist Experiment

Gold Could Offer A Way Out Of Switzerland’s Failing Inflationist Experiment8 Feb 2021

“Dirk Niepelt im swissinfo.ch-Gespräch (Interview with Dirk Niepelt),” swissinfo, 2020

“Dirk Niepelt im swissinfo.ch-Gespräch (Interview with Dirk Niepelt),” swissinfo, 202016 Dec 2020

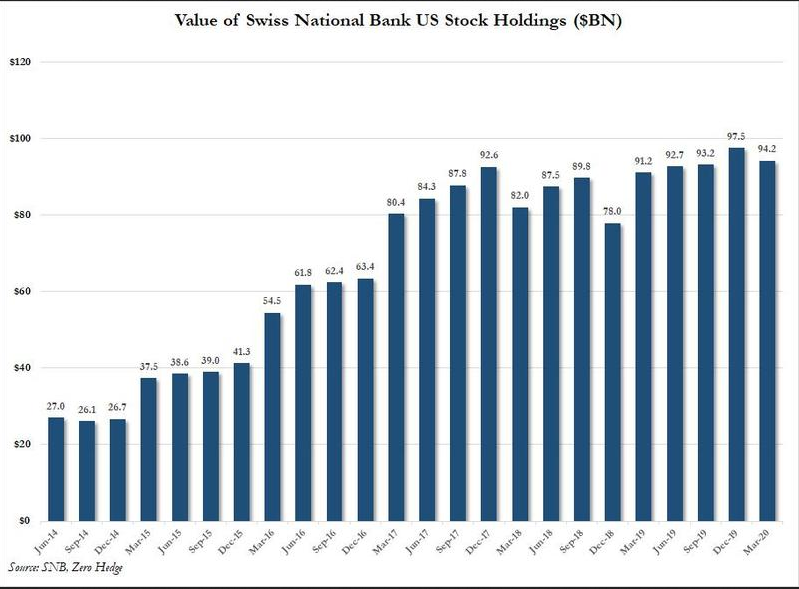

As Markets Crashed, The Swiss National Bank Went On A Tech Stock Buying Spree

As Markets Crashed, The Swiss National Bank Went On A Tech Stock Buying Spree19 Aug 2020

“Unabhängigkeit der Nationalbank (Independence of the SNB),” FuW, 2020

“Unabhängigkeit der Nationalbank (Independence of the SNB),” FuW, 202028 Jul 2020

“Monetäre Staatsfinanzierung mit Folgen (Monetary Financing of Government),” Die Volkswirtschaft, 2020

“Monetäre Staatsfinanzierung mit Folgen (Monetary Financing of Government),” Die Volkswirtschaft, 202027 Jul 2020

“Wenn die Notenbank den Staat finanziert (When the Central Bank Finances the State),” FAS, 2020

“Wenn die Notenbank den Staat finanziert (When the Central Bank Finances the State),” FAS, 20202 Jun 2020

Switzerland Peps Up SMEs

Switzerland Peps Up SMEs28 Mar 2020